TLDR (too long didn’t read): What you need to know

When completing bookkeeping, choosing the correct VAT treatment can sometimes feel confusing. The key is understanding that not every transaction with no VAT charged is treated in the same way.

This guide is designed as a practical reference point when completing bookkeeping. VAT rules can be detailed, and the correct treatment can depend on the exact goods or services involved, so if you are unsure, it is always best to check with a professional before submitting your VAT return.

Why getting VAT rates right matters

For VAT registered businesses that complete their own bookkeeping, selecting the right VAT code is an important part of keeping accurate records.

It can be tempting to think that if no VAT has been charged, the transaction can simply be recorded as “no VAT”. However, there is a difference between zero-rated, exempt, outside the scope, and reverse charge transactions.

Using the wrong VAT treatment could affect the figures included in your VAT return and may make your records harder to review.

Standard rate VAT, 20%

The standard 20% rate is the VAT treatment used most often. Unless a product or service falls into a specific category with a different treatment, the standard rate will usually apply.

Common examples of standard-rated items include:

- Accountancy and consultancy services

- Marketing services

- Office equipment

- Computers and software

- Many business purchases

For example, if a business buys a computer for £1,000 plus VAT, the invoice would normally show:

- Cost: £1,000

- VAT at 20%: £200

- Total paid: £1,200

A VAT-registered business may be able to reclaim the VAT, subject to the usual rules around VAT recovery.

Reduced rate VAT, 5%

The reduced rate applies only to certain goods and services where HMRC has set a lower VAT rate. It is not a rate businesses can choose to apply themselves.

Common examples include:

- Domestic fuel and power

- Some energy-saving materials, where specific conditions are met

- Certain mobility aids

For example, a qualifying energy supply costs £100. The invoice would show:

- Cost: £100

- VAT at 5%: £5

- Total paid: £105

The reduced rate often depends on specific circumstances, so it is important to check the rules rather than assume a product or service qualifies.

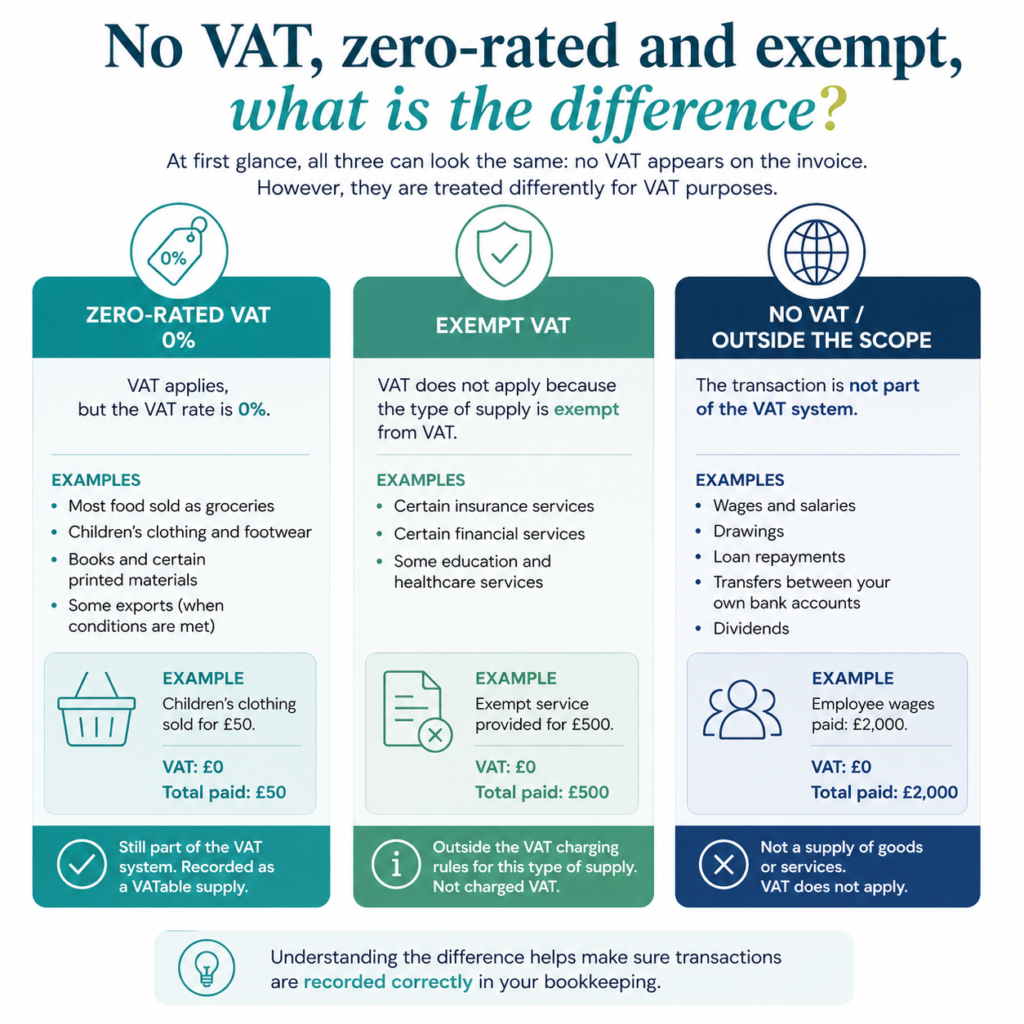

No VAT, zero-rated and exempt, what is the difference?

This is one of the most common areas of confusion when completing bookkeeping because, at first glance, all three can look the same: no VAT appears on the invoice.

However, they are treated differently for VAT purposes.

A simple way to think about it is:

- Zero-rated: VAT applies, but the VAT rate is 0%.

- Exempt: VAT does not apply because the product or service has been deemed exempt from VAT under the VAT rules.

- No VAT / outside the scope: The transaction is not part of the VAT system.

Understanding the difference helps make sure transactions are recorded correctly in your bookkeeping.

Zero-rated VAT, 0%

Zero-rated supplies are still part of the VAT system. The difference is that VAT is charged at 0%, rather than at 20% or 5%.

Examples can include:

- Most food sold as groceries

- Children’s clothing and footwear

- Books and certain printed materials

- Some exports where the relevant conditions are met

For example, a retailer sells qualifying children’s clothing for £50. The VAT treatment would be:

- Cost: £50

- VAT at 0%: £0

- Total paid: £50

Although no VAT is charged, the transaction is still recorded as a VATable supply.

Exempt VAT

Exempt means VAT is not charged because the supply is outside the VAT charging rules for that type of transaction.

In practical terms, this means HMRC has decided that certain types of goods or services should not have VAT added to them. The business does not include VAT on the customer’s invoice because that particular service or product is exempt from VAT.

The key difference between exempt and zero-rated is that zero-rated supplies are still within the VAT system, but VAT is charged at 0%. Exempt supplies are not charged VAT because the type of transaction is exempt from VAT.

Examples can include:

- Certain insurance services

- Certain financial services

- Some education and healthcare services

For example, a business provides a qualifying exempt service for £500. The invoice shows:

- Service value: £500

- VAT: £0

- Total paid: £500

No VAT or outside the scope

No VAT or “outside the scope” means the transaction is not considered part of the VAT system.

These transactions are different from zero-rated and exempt supplies because VAT does not apply in the first place.

Common bookkeeping examples include:

- Wages and salaries

- Drawings taken by a sole trader or partner

- Loan repayments

- Transfers between your own bank accounts

- Dividends

- Some grants, depending on the circumstances

- Some transactions that fall outside UK VAT rules

For example, a business pays an employee £2,000 in wages.

The bookkeeping entry records the payment, but there is no VAT because wages are not a supply of goods or services for VAT purposes.

Reverse charge VAT, what does it mean?

Reverse charge VAT is not a VAT rate. Instead, it’s a different way of accounting for VAT where the customer, rather than the supplier, is responsible for recording the VAT on the transaction.

In a standard VAT transaction, the supplier charges VAT on their invoice, the customer pays it, and the supplier then accounts for that VAT to HMRC.

With the reverse charge, the supplier does not charge VAT. Instead, the customer records both the VAT they would have paid and, if they’re entitled to reclaim it, the VAT they can recover on their own VAT return.

For many VAT-registered businesses that can reclaim all of their VAT, this often has little or no overall cash impact because the VAT is effectively accounted for and reclaimed on the same return. However, it’s still important that these transactions are recorded correctly in your bookkeeping.

Reverse charge rules only apply in specific situations. Common examples include certain services purchased from overseas suppliers and some supplies within industries such as construction, where the domestic reverse charge rules apply.

Common VAT Issues

Common Issue 1

Common Issue 2

Common Issue 3

Common Issue 1

Assuming every transaction without VAT is the same

An invoice showing no VAT does not automatically mean it is zero-rated. It could be exempt, outside the scope, or subject to reverse charge.

Common Issue 2

Choosing a VAT code based on the supplier

The VAT treatment depends on the goods or services supplied, not just who the supplier is.

Common Issue 3

Copying old transactions without checking

If a supplier changes what they provide, or the circumstances of a purchase change, the VAT treatment may also change.

Final thoughts

VAT can feel complicated, especially when different transactions appear to have the same outcome on an invoice.

The important thing is that “no VAT charged” does not always mean the same thing. Taking a moment to identify whether something is zero-rated, exempt, outside the scope, or subject to reverse charge can help keep your bookkeeping accurate.

Ready to move beyond basic accounting?

At Harland, we support clients who manage their own bookkeeping by reviewing their VAT returns, answering questions, and helping ensure VAT returns are submitted correctly. Alternatively, we can also take care of the whole process with our expert book-keepers. If you’re new to Harland, book a free discovery call to explore how we can support you.